Managing geopolitical risks: lessons from climate change risk management for supervisors

Martina Menegat and Agnieszka Smoleńska identify the common features of geopolitical and climate risks and outline how emerging prudential approaches developed in the climate domain could strengthen the management and governance of geopolitical risks in the banking sector.

Climate change and geopolitical risks are closely intertwined. Climate change is set to intensify geopolitical tensions, from shifting power dynamics in the Arctic to the effects on food security and migration patterns. Geopolitical tensions, in turn, hinder effective climate action and give rise to new arenas of geopolitical and geoeconomic competition, such as the contest over critical minerals. The interplay between climate change and geopolitical risks can thus amplify both, generating economic impacts greater than the sum of individual risks. Such compound risks can potentially undermine the soundness of individual credit institutions and broader financial stability. New macroprudential approaches are needed to address such compounding systemic risks.

Even when considered separately, important lessons can be drawn from how climate risks have been integrated into prudential frameworks globally to address geopolitical risks.

How geopolitical and climate risks compare

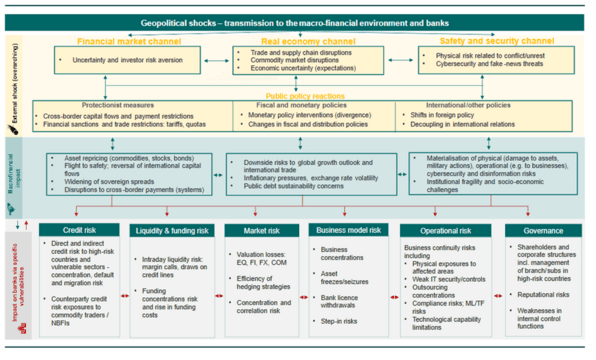

Geopolitical risks have been defined as the “threat, realization, and escalation of adverse events associated with wars, terrorism, and any tensions among states and political actors that affect the peaceful course of international relations”. Bank supervisors are increasingly realising that geopolitical factors drive risk across existing prudential categories, with this understanding growing since Russia’s invasion of Ukraine in 2022 (Figure 1 provides one way of mapping the transmission channels).

Recent research shows that geopolitical risks are not priced in by banks until they materialise, which suggests that current bank risk management is falling short (see also research for the European Parliament). However, there are currently no best practice measures or supervisory guidance for banks to manage geopolitical risks, even if prudential credit risk calculations in the Basel Framework cover force majeure events (such as wars).

Figure 1. Transmission of geopolitical shocks to the macro-financial environment and banks (Source: Buch, 2024)

Geopolitical and climate risks share several common features (see Table 1), such as a high level of uncertainty, that make them difficult to fit into existing prudential frameworks, which are typically based on backward-looking risk modelling approaches. Like climate risks, geopolitical risks are foreseeable but hardly unpredictable: they are marked by uncertainty (especially at the individual level), limited measurability and asymmetric time horizons. Although some data exists on how past geopolitical crises have affected financial stability, these historical experiences offer little predictive power in today’s deeply interconnected global markets. At the same time, the trajectory of climate risks is more predictable (and could culminate in ‘green swan’ events), as their occurrence is increasingly certain and influenced by current actions, whereas geopolitical risks remain inherently uncertain (producing ‘black swan’ events) and therefore difficult to hedge.

Table 1. Comparing climate and geopolitical risk features (Source: Authors)

| Feature | Climate risks | Geopolitical risks |

| Uncertainty | Materialisation is very likely (green swan) | Materialisation is possible (black swan) |

| Scope/range | Wide-ranging, affecting multiple sectors and regions | |

| Time horizon | Long; impacts may occur gradually or accelerate unexpectedly through tipping points | Asymmetric (short- or long-term); low predictability (events can emerge unexpectedly and escalate quickly) |

| Quantifiability | Cannot be easily quantified or modelled probabilistically (see analysis for climate here) | |

| Data availability | Absence of past records | Some historical data exist (e.g. phases of geopolitical unrest like the World Wars), showing rapid deterioration of banks’ capital ratios Data may be available to supervisors but not to the market |

| Reversibility | Irreversible, with technologies available now or in the near future | Reversible – political or geopolitical events can be resolved over time |

| Endogeneity | Partially endogenous to the financial system – financial actors amplify the magnitude of such risks with their individual behaviours and actions | |

| System effects | Non-linearity and system-wide effects due to physical changes; small changes can trigger large impacts | |

Lessons from the supervision of climate risks

Bank supervisors have invested considerable effort into developing methodologies and practices to integrate climate risks into prudential frameworks. The advancements achieved in this area can now serve as a foundation for supervisors as they confront the emerging challenge of addressing geopolitical risks. Notwithstanding the differences between climate and geopolitical risks outlined in Table 1, two key relevant regulatory innovations here are uses of scenario analysis and new governance requirements.

Firstly, supervisors have increasingly relied on diverse scenario analyses to test banks’ resilience to climate risk. Similarly, developing a set of geopolitical scenarios, adapted to regional and national contexts, can help supervisors to identify which geopolitical developments are most likely to impact the banking sector and financial markets. The European Central Bank (ECB) has already announced that in 2026 it will conduct a thematic stress test on geopolitical risks. Scenarios fit for geopolitical scenarios might focus on specific (sectoral) transmission channels (e.g. disruption of supply chains; energy security). Methodological advancements in climate risk assessments, including nature scenarios, which take a more localised view, can serve as a blueprint for supervisors to examine how geopolitical shocks and their transmission channels may influence banks’ solvency and profitability.

Secondly, the integration of climate risks into prudential frameworks has also largely focused on embedding these risks into bank governance structures, including through new resilience-enhancing tools such as transition plans. A similar approach could be applied to supervisory guidance on geopolitical risks, requiring, for instance, a clear allocation of responsibilities and roles across business lines and risk management functions (e.g. cross-functional points of contacts); a well-defined framework for identifying geopolitical risks from both a financial and non-financial perspective; and the integration of geopolitical considerations into the fit and proper assessments of management board members and senior managers.

Future pathways for research and policy investigation

There are several areas for future research where geopolitical risks may extend beyond the current state of the art in integrating climate risks into the risk management practices of banks.

First, supervisors increasingly need to face multiple risks that have broad societal implications, which amplify each other through feedback loops. This creates the risk of burdensome, multiplying yet siloed supervisory assessments and expectations. There is a need to integrate compounding risks into a single framework. The short-term climate scenarios from the Network for Greening the Financial System (NGFS) show how this can be done: constructed in the aftermath of the Russian invasion of Ukraine, they integrate energy security implications into climate transition pathways.

Second, central banks and financial supervisors increasingly recognise that climate (as well as nature) risks are partially endogenous to the financial system Banks’ financing choices (asset allocation; lending practices; market reactions) may amplify these risks due to the collective behaviour, incentives and market dynamics within the financial system, generating feedback effects that impact both individual institutions and the stability of the wider financial system (so-called ‘double materiality’). Typically, geopolitical risks are seen as exogenous to the financial system. However, future research could investigate how geopolitical risks may be partially endogenous, for instance through banks’ engagement with their strategies’ sectoral or geographical dependencies (e.g. in the context of value chains that are dependent on rare-earth minerals).

Positive social and governance impact may help address some of the factors underlying geopolitical tensions. From that perspective, a double materiality logic developed for climate risks could help better anticipate and, at the right moment, mitigate geopolitical vulnerabilities. This could involve, on a case-by-case basis, encouraging or requiring institutions to develop preparedness plans or set limits to tackle certain geopolitical exposures. Some supervisors, such as the ECB, have already taken steps in this direction, asking banking institutions to scale down their presence in Russia due to compliance and financial risks.

Addressing these challenges requires an evidence-based understanding of geopolitical risks as cross-sectional drivers of prudential risk categories and their links to climate risks. As supervisors must manage these interconnected challenges amid declining multilateral cooperation, further research is needed to fill knowledge gaps and inform supervisory practices globally and at the national level.

Climate change and geopolitical tensions increasingly interact, creating compound risks that can amplify shocks to banks and financial stability. Because both types of risk share features such as uncertainty, non-linearity and limited quantifiability, supervisory tools developed for climate risks, especially scenario analysis and strengthened governance expectations, can inform supervision and improved management of geopolitical exposures. Future supervisory and research efforts should integrate these compounding risks into unified frameworks, explore their partial endogeneity to the financial system, and develop evidence-based guidance to address emerging prudential vulnerabilities.